Worried about your required minimum distribution (RMD, aka minimum required distribution, MRD)? Don’t be. Fidelity’s got you covered. Here are the answers to some frequently asked questions regarding RMDs.

General information

Calculating your MRD

- How do I calculate my MRD?

Generally, your MRD is determined by dividing the adjusted market value of your tax-deferred retirement account as of December 31 of the prior year by an applicable life expectancy factor taken from the Uniform Lifetime Table (PDF).

Our MRD Calculator

can help you determine what to withdraw. We also offer the Retirement Distribution Center which can help you manage your withdrawals. This free service keeps track of how much you’ve withdrawn to date, allows you to set up automatic withdrawals, and provides estimated MRDs for your Fidelity IRAs (Traditional IRAs, SEP IRAs, SIMPLE IRAs, Rollover IRAs, and all small-business retirement plans). Learn more about our Retirement Distribution Center.

- What if my spouse is more than 10 years younger?

If your spouse is more than 10 years younger than you, and if he or she will be the sole primary beneficiary for the entire distribution year, you should use the Joint Life Expectancy Table (PDF) to calculate your MRD. This will result in a smaller MRD than with the Uniform Lifetime Table. You can use the MRD Calculator

- Will Fidelity calculate my MRD for me?

Yes, to view your MRD estimate for the current year, please visit the Retirement Distribution Center (RDC)Log In Required. You can also find current year estimates and year-to-date withdrawals on your account statement. Prior year estimates, dating back to 2012, are available in the RDC but only for accounts held at Fidelity during that time.

Please note, we calculate your MRD based on a variety of factors such as your date of birth, year-end account balance, and account beneficiaries. If any of this information changes, your Fidelity-provided MRD may no longer be accurate.

The MRD estimates use all the information on file as of December 31 of the prior year. For example, transfers that are not processed by December 31 will not be be reflected in the next year’s MRD. So, if you transfer funds to your retirement account in late 2015, but they are not received by December 31, 2015, your 2016 MRD will not reflect this deposit. Similarly, beneficiary changes made after December 31 will not be reflected in the current year MRD.

If you have consolidated assets, transferred funds, or made a beneficiary change that should have been taken into consideration for the current year, please call our representatives at 800-544-4774 for help recalculating your MRD.

Please note, MRD estimates for Fidelity’s Profit Sharing Retirement Plan, Money Purchase, and Self‐Employed 401(k) accounts, are presented separately and not aggregated in the All Your Fidelity IRAs section of your portfolio.

Additionally, 401(k), 403(b), and 457 plans held at Fidelity and certain annuities are not included in the MRD estimate. To learn more about how we estimate your MRD, please visit the RDC and select Learn more about your MRDs and how they’re calculated.

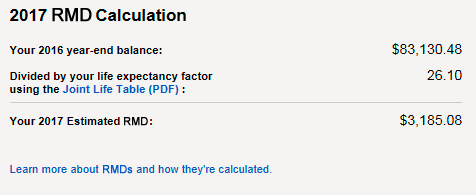

Sample RDC calculations page:

- Where can I find the Retirement Distribution Center?

You can visit the RDC directly at www.fidelity.com/RDC Log In Required. It can also be found on the Track Your Minimum Required Distributions (MRDs) section of your account summary that appears after you log in.

Note: This information is only visible to those with required withdrawals. If you’re under 70 ½ or do not own an Inherited IRA account, you may not see the card.

If you own an Inherited IRA and are under 70 ½, you may still have required withdrawals. Learn more about MRDs for inherited retirement accounts

If you have required withdrawals but do not see an MRD estimate, we may be missing key information such as your prior year’s account balance and date of birth. If that’s the case, please update your account.

- Will Fidelity send me my MRD automatically?

Yes, if you enroll in our automatic withdrawals process, Fidelity will automatically recalculate your MRD each year, and distribute that amount based on your instructions. Enroll in automatic withdrawals

.

Beneficiaries and stretching tax advantages of assets

- How do I name a beneficiary?

A designated beneficiary is an individual, charitable organization, estate, or other entity that you have named to receive any assets in your account upon your death. Update your beneficiaries

You may also complete a beneficiary form.

- Should I convert to a Roth IRA, since they don’t have MRDs?

You can convert a Traditional IRA to a Roth IRA at any age. If you are over age 70½ when you convert, you will need to take your MRD for the Traditional IRA before converting any other amounts into the Roth IRA. Our online Convert an IRA to a Roth IRA