You’ve heard about the supposed “death of the balanced portfolio.” Now, explains Jason Zweig, researchers want to declare bonds non grata in your portfolio forever. For them, there is no alternative (TINA) to stocks. Zweig explains:

Tina stands for “there is no alternative.” Years ago, when interest rates were near zero and investors were acting as if stocks were the only choice, market strategist Jason Trennert of Strategas Research Partners popularized the term “the Tina market.”

The latest argument for Tina comes from a newly updated analysis by a team of researchers who find that retirement savers shouldn’t own any bonds at all.

Instead, according to this line of reasoning, investors should keep one-third of their savings in U.S. stocks and two-thirds in international stocks. The researchers advocate that you should hold all stocks, all the time—not only when you’re young and saving for retirement, but even after you retire, for as long as you live.

If only stocks were a sure thing. In financial markets, nothing ever is. You can’t just take an analysis of the past, no matter how careful it is, and assume you can extrapolate it into the future.

To reach their conclusion, Scott Cederburg, a finance professor at the University of Arizona, and his colleagues Aizhan Anarkulova at Emory University and Michael O’Doherty of the University of Missouri, analyzed stock and bond returns from 39 countries from 1890 through 2023, taking the longest available period during which each was classified as a developed market. That’s up to 134 years for such markets as the U.S. and the U.K., and as short as four years for Colombia.

Their central finding, across the decades and around the globe: Bonds have historically tended to go up and down in sync with stocks over long periods, making them poor diversifiers—while offering low returns, to boot.

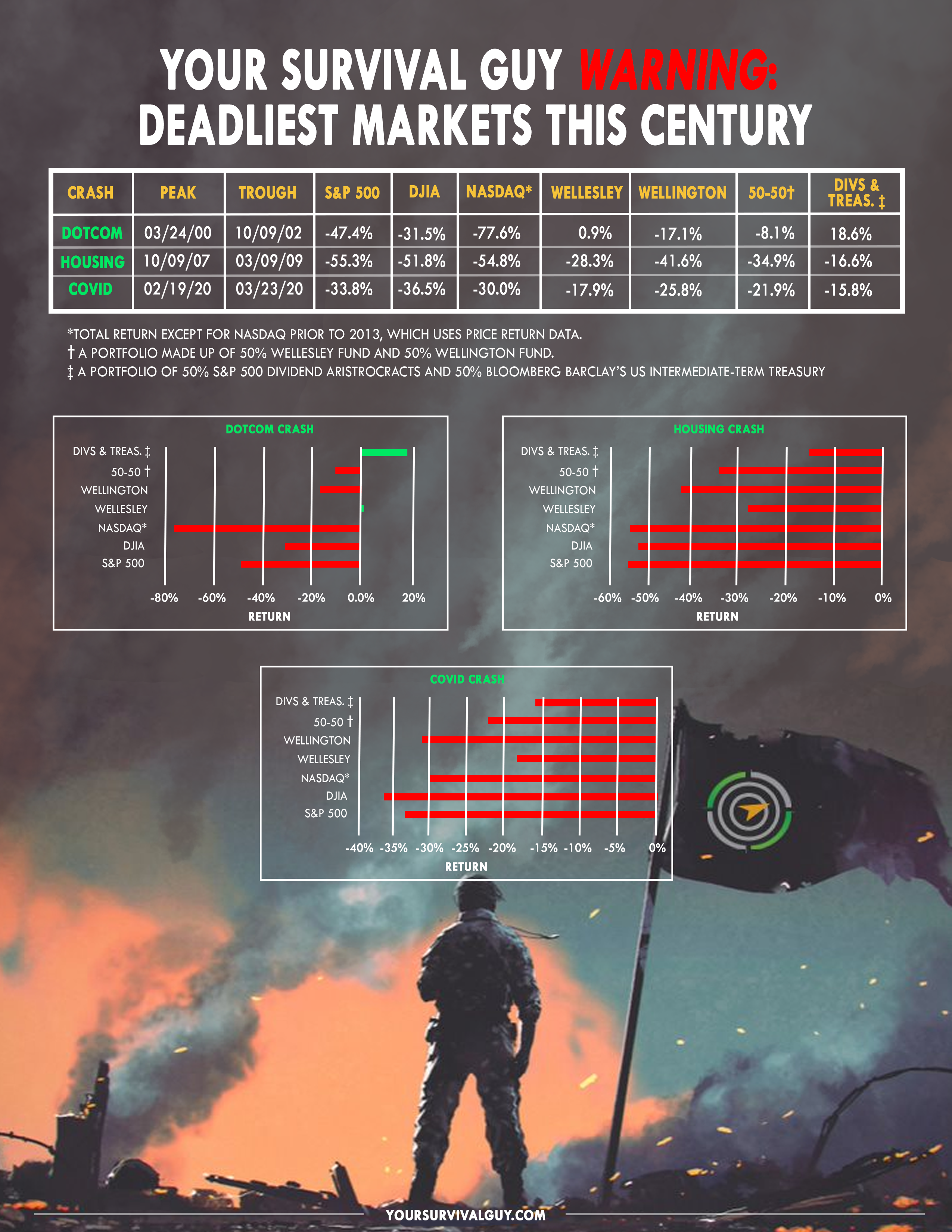

Despite what the researchers say, investors who owned bonds during the three deadliest markets this century were probably happy with their decision. Look at the devastation the stock market has endured multiple times in just the last 25 years:

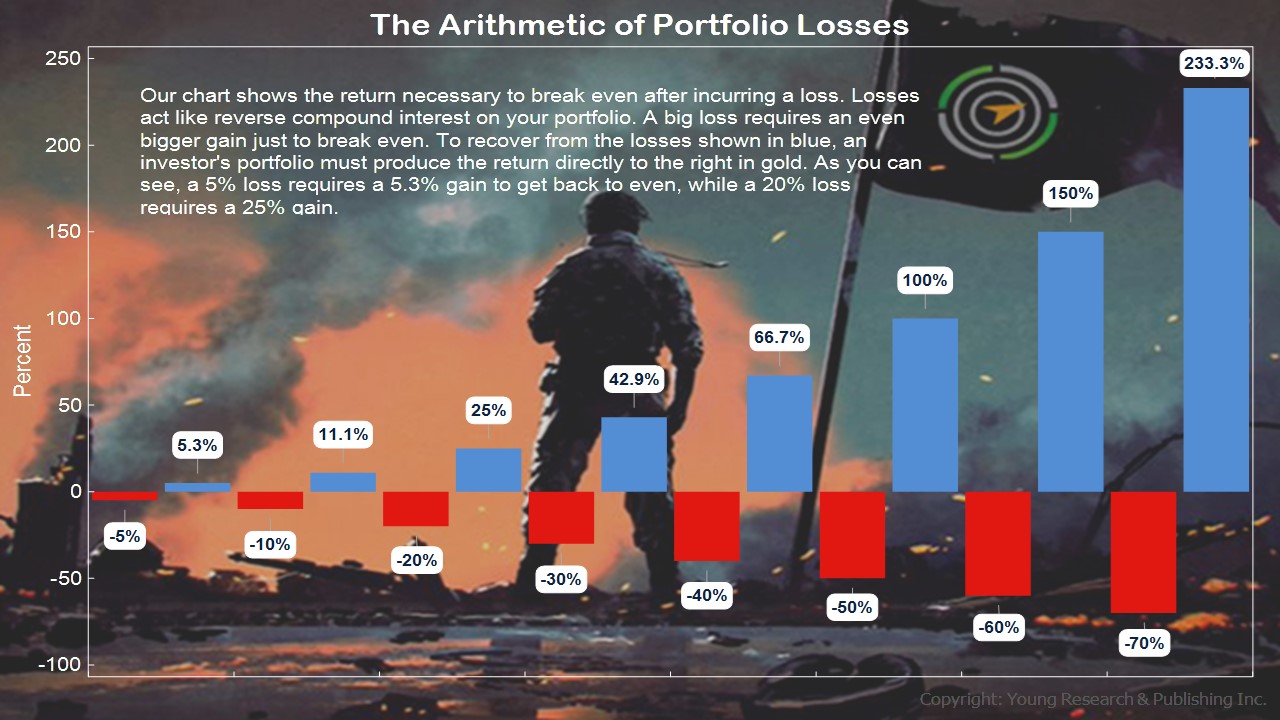

In the above graphic, you can compare the performance of balanced portfolios to all stock portfolios. If you had started your retirement the day before any of these crashes hit, which portfolio would you have preferred to own? The thing about losses is that they take further gains just to get you back to even. Take a look at the arithmetic of portfolio losses below:

Action Line: It’s a pretty bleak picture if you suffer catastrophic losses early in your retirement. When you want to talk about a balanced portfolio approach, email me at ejsmith@yoursurvivalguy.com. And click here to subscribe to my free monthly Survive & Thrive letter.