You may have read my recent series on Vanguard Wellington, and your ability to own the fund at Fidelity. You can have your cake, and eat it too by owning a balanced fund at my favored custodian. If you read the series and enjoyed it, be sure to send this post along to anyone you know who could benefit from it. And if you want to talk more about building a personalized balanced portfolio of stocks, bonds, and precious metals, I’m here. That’s the icing on the cake.

Your Vanguard Wellington Fund’s Outlook

Is your Vanguard Wellington fund’s outlook OK? In a word, yes. But before we get into my favorite balanced fund, let’s remember it’s not managed by Vanguard. It’s managed by Wellington Management up in Boston, the home base of my favored Johnson family’s Fidelity Investments and the epicenter of old-monied firms like Brown Brothers Harriman.

My father-in-law Dick Young would call on Wellington during his days in Boston. And remember, Vanguard founder Jack Bogle was a Wellington Management guy. The money management business has deep Boston roots.

As an aside, it’s my belief that Bogle’s mistreatment by Vanguard began when he was put out to pasture at the annex at the company’s Malvern, PA, headquarters campus. The founder of the company literally stationed a building away from the C-suite. The writing was on the wall as Vanguard was becoming too big, hence my current-day concerns.

But the good news is that you can have your cake and eat it, too. You can keep your Vanguard Wellington fund and transfer it to my favored greener pastures at Fidelity Investments.

Consolidating your assets without selling, or an in-kind transfer to Fidelity, is like going grocery shopping for your consumer staples. You can get them anywhere, but the customer experience will differ from one store to another. It’s why I like the gold standard custodianship at Fidelity for your money.

Let’s talk about moving your investments to Fidelity and building a balanced portfolio with a plan for the long-term. When you’re ready, I’m here.

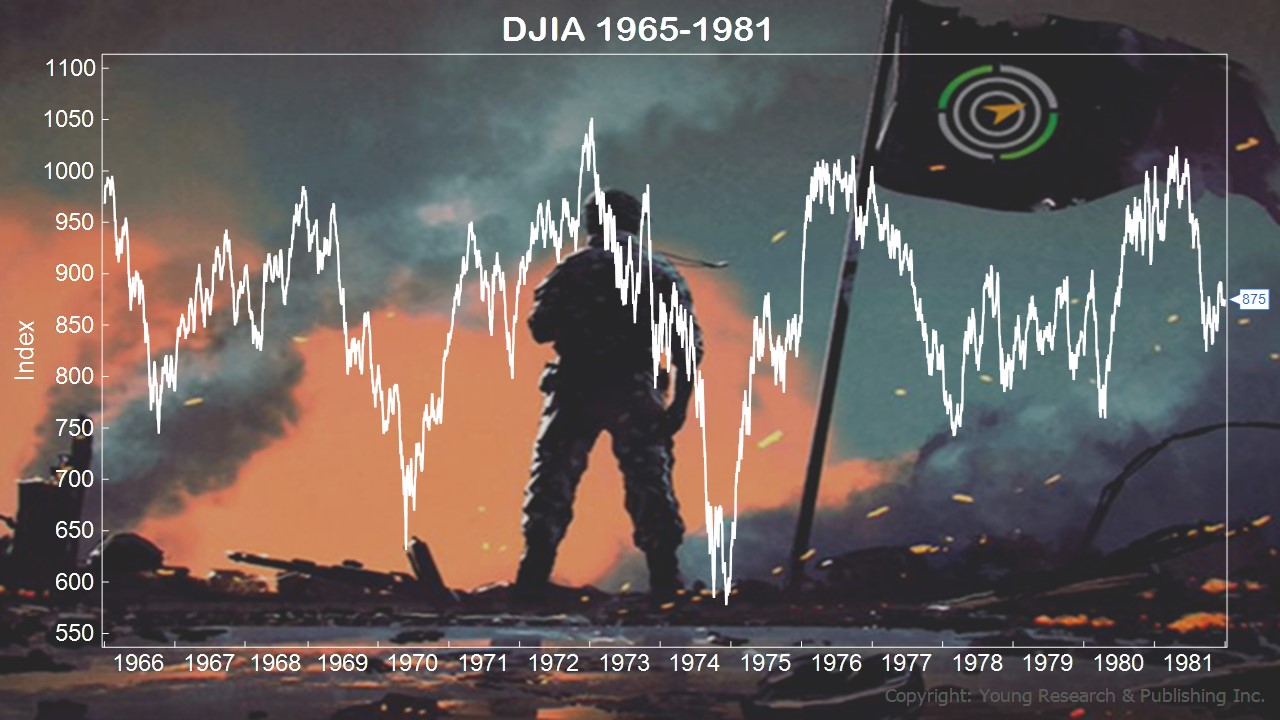

That ‘70s Show All Over Again?

You’ll want to draw your attention to the recent mini blip in stocks. Imagine if it lasted decades instead of days. How would you feel if we had a redo of that ’70s show?

What I want you to focus on today is a performance comparison during the mini blip of Vanguard’s Wellington fund vs. the S&P 500. As you can see in the chart below, Wellington held up nicely.

You know my concerns about Vanguard. The good news is you can have your cake and eat it, too by transferring in-kind—not selling your Wellington Fund—to my favored Fidelity Investment. Remember, sometimes the destination makes all the difference in your experience. I’m here when you need me. But only if you’re serious.

When You Should Be a Buyer, not a Seller

Is your Vanguard Wellington fund’s outlook, OK? In a word, yes. But what does that mean for investors in the fund? You know you can have your cake and eat it too. In other words, you can keep your Wellington and transfer it to Fidelity Investments.

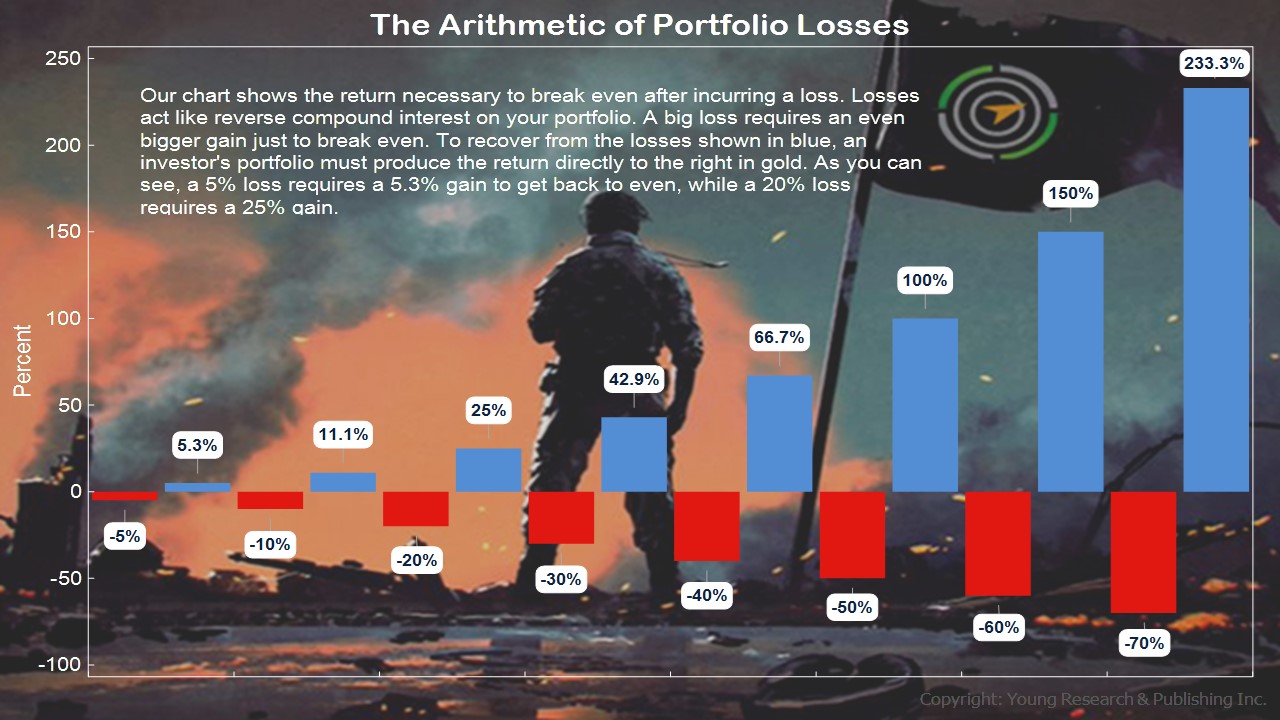

But let’s step aside for a moment and consider how investors sell at the worst of times because they can’t handle losing money. When they capitulate and throw in the towel, it’s more about how much money they can’t stand to lose. It has nothing to do with the future. And, of course, history shows these are the times to be buyers, not sellers.

The beauty of the Vanguard Wellington fund is its balanced approach. It’s a mix of around 40% in bonds and around 60% in stocks. What history shows is the balanced approach helps lessen the wild swings in stocks. When it comes to your retirement life, you do not want to be worried about your money. “How much did we lose today?” asks your spouse. This is not a question I want you to receive.

Being worried about anything is a terrible emotion. I don’t want you to be worried about your money. If investors focused more on their downside protection than on how much they need from the market, I believe they would be less worried. They would live within their means and not hope for miracles from the market. But they tend to learn the hard way.

Action Line: Focus on your downside protection. Save ‘til it hurts. Work for as long as you can. And live within your means. Simple, yet hard for many to do. If you want to talk, let’s talk. But only if you’re serious.