Judging by the popular CAPE ratio, investors are paying prices for earnings from publicly traded companies near their all-time highs. Jason Zweig reports in The Wall Street Journal:

Robert Shiller, a finance professor at Yale University, who won a Nobel Prize in economics in 2013, measures how expensive stocks are by taking the price of the S&P 500 index, dividing by the average of its past 10 years of earnings and adjusting both the price and the earnings for inflation.

The gauge is known as the cyclically adjusted price/earnings ratio, or CAPE. And, by that yardstick, stocks were priced at 20.3 times their adjusted long-term profits at the beginning of 2010. The average valuation for U.S. stocks over the full historical sweep of Prof. Shiller’s data, all the way back to 1881, was then 16.3 times their adjusted earnings.

That meant that stocks were priced nearly 25% above their historical average. This led me to believe their returns over the coming decade were bound to be lower.

Over the next 10 years, earnings boomed, but the price investors were willing to pay for those earnings boomed even more.

Today, at a CAPE of 37.1 times adjusted earnings, stocks are significantly above their early record of 32.6 in September 1929 and not far from their all-time high of 44.2 in December 1999.

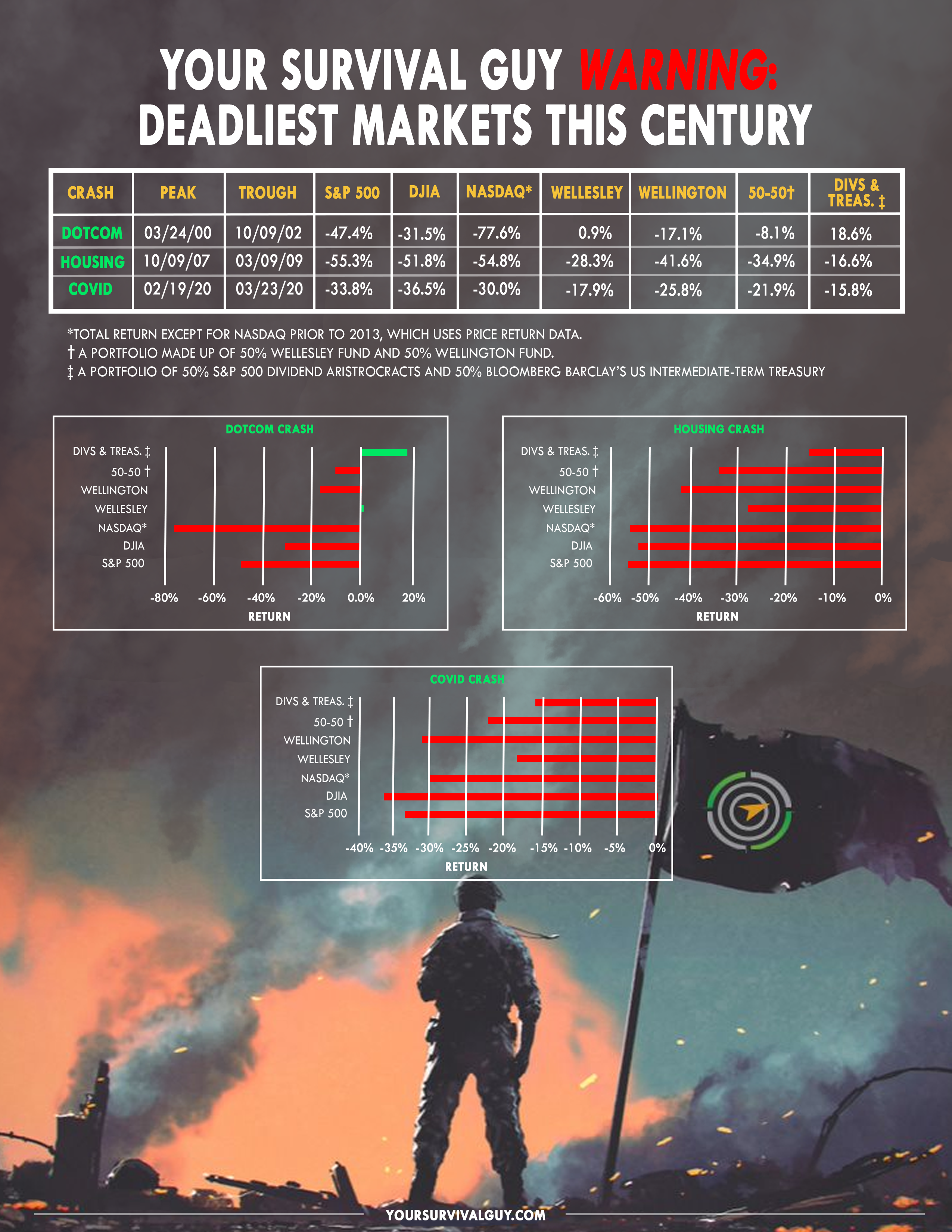

Both peaks ushered in devastating bear markets, with stocks losing more than 80% between 1929 and 1932, and more than 40% between the end of 1999 and late 2002.

Action Line: Make sure you’re prepared for the worst markets. If you need help building a portfolio with market bubbles in mind, I would love to talk with you. If you would like to get to know me before we talk on the phone, there’s no better way than signing up for my free monthly Survive & Thrive letter. In the letter each month, I encourage and push you to achieve the personal and financial security goals you’ve set for your family. Click here to subscribe. We’ll get to know each other, and get serious about your future success.